GBI 100% Income Tax Exemption and Stamp Duty Allowance (2009-2014)

Since the inception of Green Building Index in 2009, the Malaysia government has introduced various strategies under Budget 2010 (excerpts HERE). Aside from rebranding Pusat Tenaga Malaysia (Malaysia Energy Centre) to National Green Technology Centre and an allocation of RM20 million to spur green activities, the National Green Technology Policy was also launched. This NGTP led to the requirement of green standards in government procurements and establishing funds and loans to support green products and technology. One important motivation for the green building industry is that any certified green building project can obtain 100% tax exemption on additional capital expenditure to get the said certification. Furthermore, this can

One important catalyst for the green building industry is that any certified green building project can receive 100% tax exemption on additional capital expenditure to get the said certification. Furthermore, this can be used to set off against 100% statutory income. Secondly, buildings & residential properties owners are eligible for stamp duty exemption based on the additional cost to obtain GBI certification. Both of these, are effective from 24 October 2009 till 31 December 2014.

New Tax Incentive Workshop at Johor Bahru October 2016

This is slightly late to update though, but I have just participated the new tax incentive briefing (2014-2020). The workshop, a collaboration of Green Building Index and MIDA (Ministry of Investment Development Authority), briefly introduces the new tax incentive for green building and the specific details of Qualifying Capex for architectural elements and M&E items.

Screen Shot of MIDA Powerpoint Presentation at Tax Incentive Workshop @ Johor

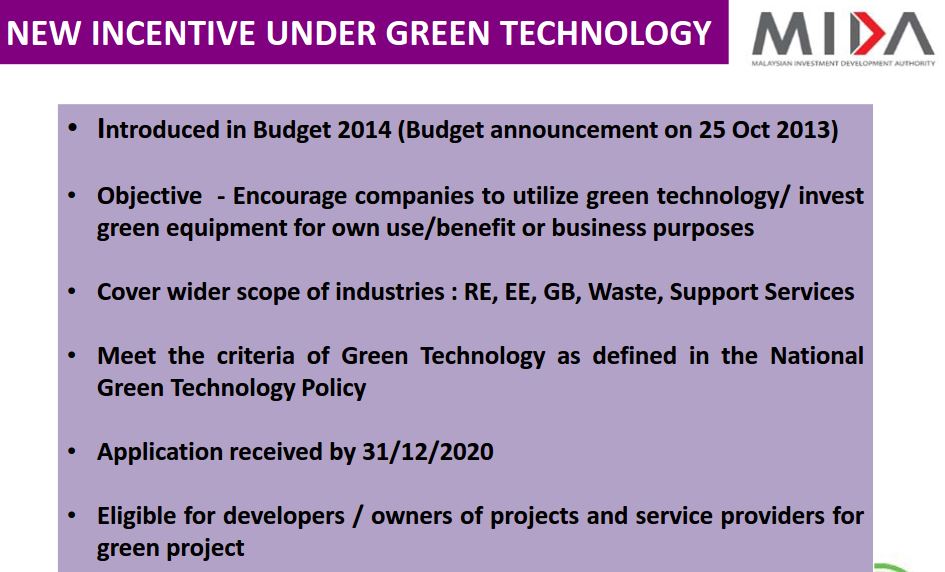

Major Updates on Green Technology Tax Incentive (2013-2020)

It is more than an incentive scheme to promote green building but green technology as a whole. You may ask what do we mean by “Green Technology”, but MIDA has spelt out distinctively for different segments of the industry in their document (but still vague in my opinion).

“The development and application of products, equipment and systems used to conserve the natural environment and resources, which minimises and reduces the negative impact of human activities”

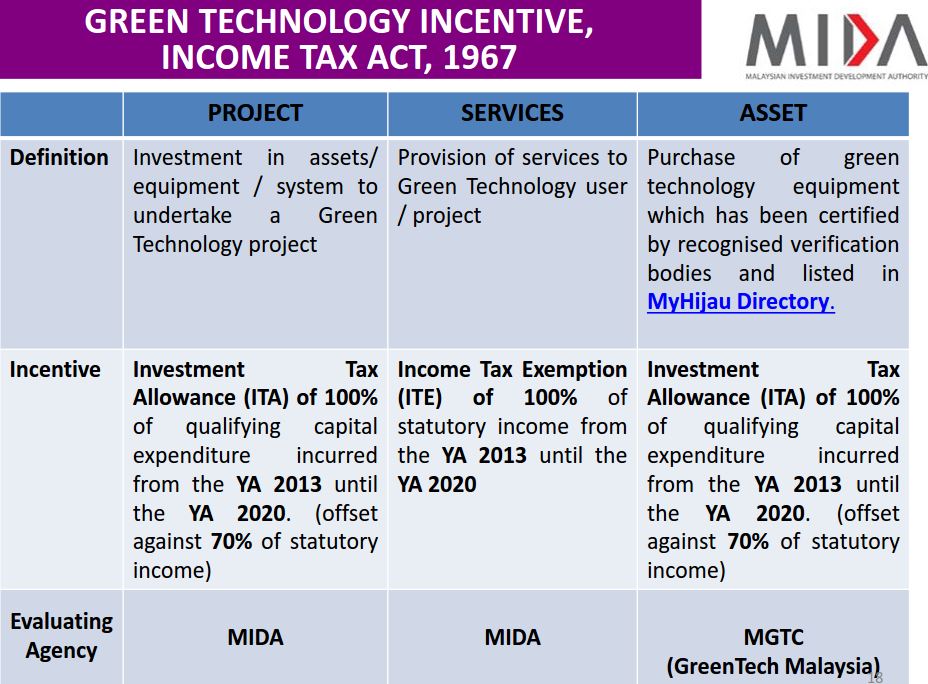

It’s general enough to holistically include different sectors but subjected to a lot of manipulation. Anyway, the tax incentive now covers the wider scope of industries, such as renewable energy, energy efficiency, green building, waste management and support services. Yes, you read “Services”! The latest Green Technology Incentive under the Income Tax Act 1067 now covers Project, Services and Asset.

Screen Shot of MIDA Powerpoint Presentation at Tax Incentive Workshop @ Johor

It’s encouraging because I think it’s much holistic to further encourage growth across all different sectors. It’s also a great push for MGTC (GreenTech Malaysia) to push for the listing of more products under MyHijau Directory. Another great thing is that the ITA and ITE is applicable for statutory income from 2013 till 2020, which definitely gives the industry player a breath of relief for quite some time. However, the catch is that the 100% Investment Tax Allowance (ITA) (For Projects and Assets) is that the total sum can be only offset against 70% of statutory income. Well, so government also wants to collect the remaining 30%! A quick example is as seen below, where you can view through the presented slides at the end of this post.

Screen Shot of MIDA Powerpoint Presentation at Tax Incentive Workshop @ Johor

The slides also further explained the terms and conditions of eligibility for such funds, the application process and the documents required. There is also an interesting section briefing on Green Technology Financing Scheme (GTFS) at the end of the slides by MIDA. Following on, GBI explained the Qualifying Capex for the different items and best practices of submission, which I will not go into details as they are all in the slides below. GBI also took opportunity in emphasising QS to refer to the uploaded worked examples on GBI green cost submission, which you can find it HERE. However, TL Chen took some real opportunity to reinforce that it is not expensive to go Green, in fact, a business economic common sense. I wrote a piece on the 5 myths of Green Building and one of them is that “Green Building is Expensive!“

Screen Shot of GBI Powerpoint Presentation at Tax Incentive Workshop @ Johor

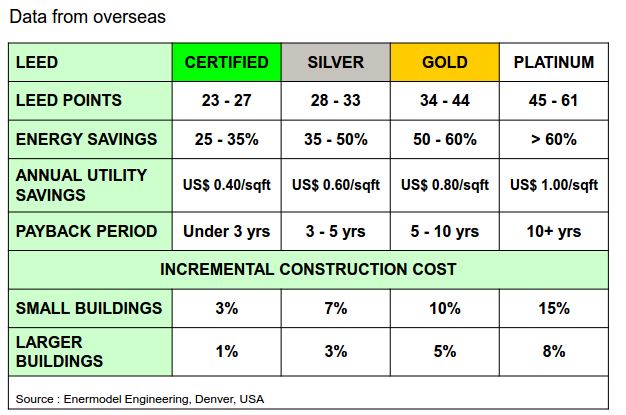

Cheaper and Common Sense to go Green

Screen Shot of GBI Powerpoint Presentation at Tax Incentive Workshop @ Johor

So TL Chen was comparing the data from overseas (LEED) and locally available in terms of cost incremental along the different level of certifications. In my opinion, this is accurate and sometimes, it doesn’t even cost to go for certified as it’s merely a good practices compliance for green building. In fact, many projects are using MS1525 and local code compliance as base cost today. Let us remember that the holistic approach of green building is always about reducing energy consumption first with the lowest hanging fruit which are mostly related to passive design instead of plucking in high efficiency M&E equipments. The typical expensive ball park figure for Silver and Gold are high performance glazing and high efficiency ACMV equipment. While for Platinum, you can expect a longer ROI items such as MERV13 for air filtration, black water treatment system and daylight strategy devices.

Tax Incentive Allowance for GBI project or Green Building project?

This is probably one of the confusion in the green building industry. On whether MIDA approves tax incentive allowance for only GBI certified project, or other any green building assessment certified projects, this has been a question where many developers depend on to evaluate their certification preference. Well, you may argue that it is not always the case for built and sell projects because they are not the end beneficiary in that case. However, back in 2009, it was GBI that pushed the ITA for green building with MGTC. I am not sure about years back then but this is a question I have asked during the workshop to both GBI and MIDA to clear the air.

We know that there are multiple green building assessment tools in Malaysia (GBI, LEED, Green Mark, GreenRE, MyCREST). Yes, that many! The clear answer is that MIDA does not specify which green certification but falls back to the general definition of green building. Let us be clear that MIDA is the final evaluating agency and not GBI. I did get an answer from GBI that we need to support the local green building rating tool (GBI), but my rational of asking this question is that I am pro green building and not pro green building rating tool. And, as a green building consultant, it is ultimately the client’s choice of which green building assessment tool to go for due to various reasons. Let’s face it there’s a marketing reputation behind various tools such as internationally recognised LEED and Green Mark.

With all due respect, I admire how long has GBI come along to establish itself since 2009 to the professionalism it is today, especially when you have professional consultants from PAM and ACEM driving the rating tools as how they know what is best for it to drive the benchmark of green building designs in Malaysia. GBI has gone long way into reaching out different stakeholders including the educational institution to hold research conference and its involvement in World Green Building Council to help Indonesia to formulate their tools. Then, there’s this familiar, convenient myth that GBI copied LEED, which has totally obsoleted because MGBC took a long consideration on each credit individually on what’s best to drive respective segments.

I think the most important thing to note is that GBI is established, same goes to GBI Accreditation Panel who reviews the QS submission for Green Cost. Hence, there’s a reputation advantage when you submit to MIDA for GBI certified projects as the submissions will be filtered by GBI before reaching MIDA, unlike other green building assessment team which do not have a reputable panel to oversee this.

For the full slides on MIDA’s presentation on the newly gazetted ITE and ITA, please download HERE or view below.

For the full slides on Qualifying Capex (QE) on M&E item, please download HERE or view below

For the full slides on QS Practice Notes on Qualifying Capex (QE) on non M&E items, please download HERE

{kind=link}